- Understanding Your Roof Insurance

- Understanding How You Get Paid

- File Your Claim The Right Way

- Review And Supplement The Estimate

- What To Expect From Your Insurance Payout

- FAQs

You walk into your living room and notice a brown water stain spreading across your ceiling. Or maybe you’re standing in your driveway after last night’s Santa Ana winds, looking at tiles scattered across your yard. A roof replacement in Los Angeles can easily cost $15,000 to $35,000 or more.

If a covered event caused your roof damage, your homeowner’s insurance might pay for most or all of it. The challenge is knowing how to get insurance to pay for roof replacement without making costly mistakes that could get your claim denied.

After 20 years of helping Southern California homeowners navigate the insurance process, we’ve learned what works and what doesn’t. This guide walks you through exactly what you need to know.

Key Takeaways

- Insurance may cover roof replacement when damage is sudden and caused by a covered event.

- Understanding your policy, RCV vs. ACV, can save you thousands of dollars.

- Documentation is everything: photos, videos, timestamps, and weather reports matter.

- Always get a professional inspection before filing a claim to avoid unnecessary denials.

- Having your contractor present during the adjuster visit protects your claim.

- Most insurance estimates miss items, while supplements help you recover the full amount owed.

- Financing options exist if your policy only pays depreciated value or your claim is denied.

Understanding Your Roof Insurance

Understanding your roof insurance policy is the first step to knowing what it will actually pay for. Not all policies work the same, and the difference between full replacement coverage and depreciated value can mean thousands of dollars out of pocket. This section breaks down what you need to look for before you file a claim.

Understanding Your Policy

Whether insurance will cover roof replacement comes down to what type of policy you have. This is the most important thing to understand.

Replacement Cost Value (RCV) is what you want. This policy pays the full cost to replace your roof at today’s prices. You’ll get two checks: the first covers the actual value minus your deductible, and the second covers the recoverable depreciation after your new roof is installed. For example, on a $25,000 roof with a $2,000 deductible, you might get $15,000 upfront and $8,000 after completion.

Actual Cash Value (ACV) is what you don’t want. This only pays the depreciated value of your roof. If you have a 20-year-old roof with a 25-year lifespan, you might only get 20% of the replacement cost. You’ll pay the rest out of pocket, often tens of thousands of dollars.

Most California policies are RCV for roofs under 15 years old, but you need to check yours. Call your insurance agent and ask specifically: “For my roof, which one do I have,e replacement cost or actual cash value coverage?”

Document Everything

The moment you notice damage, grab your phone and start taking photos. Insurance companies need proof that the damage was sudden and caused by a covered event, not something that has been worsening for years.

From the safety of the ground, photograph missing or cracked tiles, damaged flashing around chimneys and vents, dented gutters, and any obvious impact points. Take wide shots showing the whole roof and close-ups of specific damage.

Also, document what we call “collateral damage”, evidence that a storm hit your property. This includes dents in your AC unit, garage door, or downspouts, damaged window screens, marks on painted wood, and broken tree branches. If your neighbors have damage too, that helps prove a widespread weather event occurred.

Inside your home, photograph any water stains on ceilings or walls, attic dampness, and damaged insulation. Take both photos and videos with timestamps enabled.

Save weather reports from the day the damage happened. Screenshot news articles about the storm. Note the exact date, time, and conditions. All of this builds your case that this was a sudden, covered event.

Warning: don’t go on your roof yourself. It’s dangerous, and if you fall and get hurt, your insurance might not cover that either. Let the professionals handle the roof inspection.

Get A Professional Inspection First

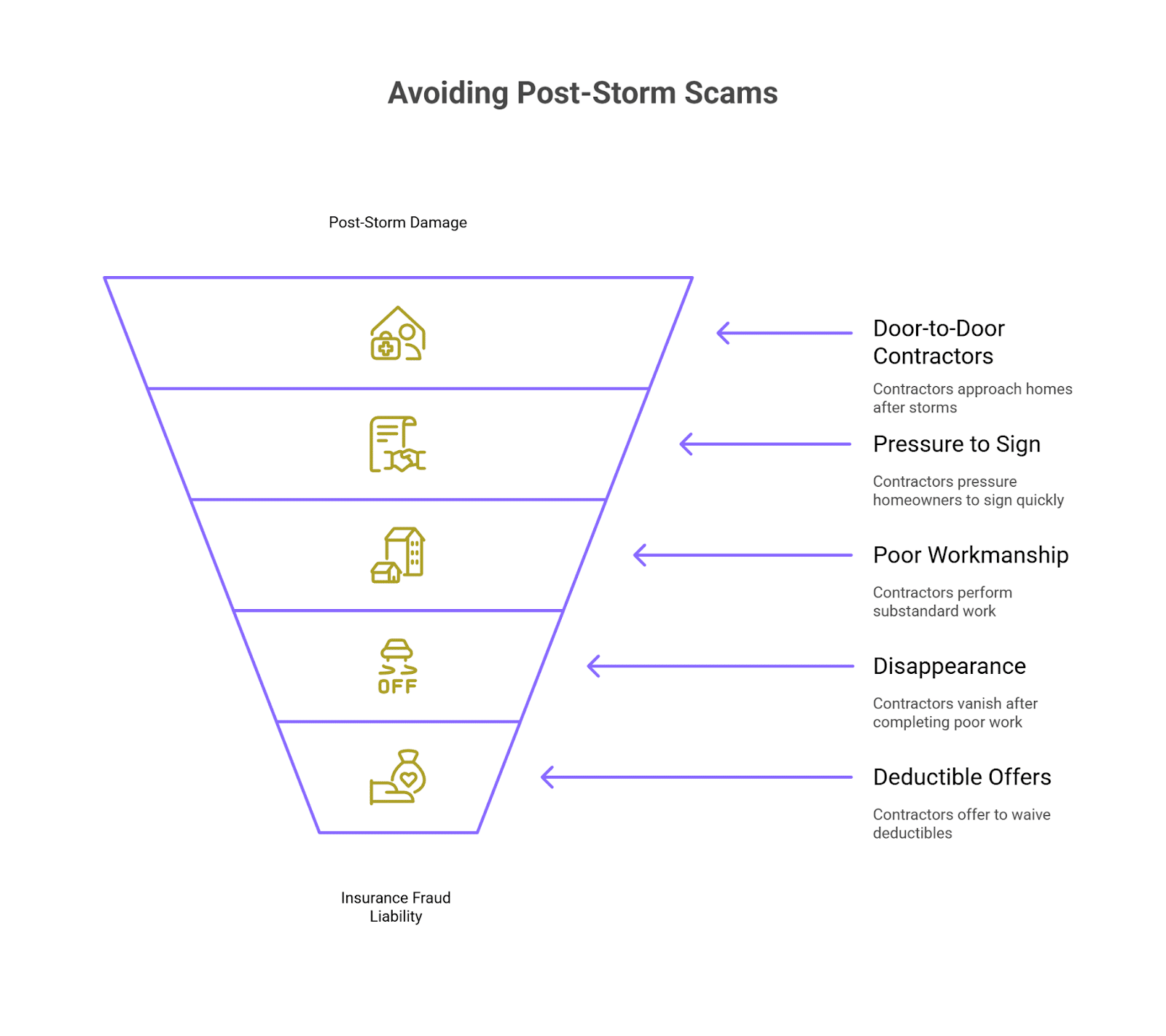

Here’s where most homeowners make a mistake. They call their insurance company first, then look for a contractor. Do it the other way around.

Why? Because you need to know if you have a viable claim before you file. Once you file that claim, it goes on your record even if it gets denied. A professional inspection tells you whether the damage is significant enough and clearly storm-related enough to be worth filing.

A reputable roofing contractor will come , assess the full extent of damage (including hidden issues you can’t see), take professional photos and measurements, and give you an honest opinion about whether you should file a claim. They’ll also provide a detailed estimate that you’ll need anyway.

When choosing a contractor, look for someone who is licensed and insured (verify with the California Contractors State License Board), has experience working with insurance claims, has strong local reviews, and offers a free inspection.

Not sure if your roof damage qualifies for a claim? Getting a professional opinion first can save you time and money.

Get a free quote

File Your Claim The Right Way

Once you’ve confirmed you have viable damage, it’s time to contact your insurance company. Most policies recommend filing within 30 to 60 days of the damage, though California law gives you a reasonable time.

When you call, have your policy number ready and be prepared to explain what happened, when it happened, and what damage you’ve found. They’ll assign you a claim number and tell you the next steps.

Follow up your phone call with an email that includes all your photos, your contractor’s inspection report and estimate, and any weather reports or news articles about the storm. Keep detailed notes of every conversation: date, time, who you spoke with, and what was said.

An insurance company expert will come to inspect your roof, usually within 3 to 7 days. After major storms in Southern California, expect delays as adjusters get backlogged.

The Insurance Adjuster Visit

This is one of the most important moments in learning how to get insurance to pay for roof replacement. The adjuster works for the insurance company, not for you. Their job is to assess damage while keeping costs down for their employer.

That’s why you absolutely need your roofing contractor present during the inspection. Your contractor knows what to look for, can point out damage the adjuster might miss, and keeps the inspection honest and thorough.

During the visit, the adjuster will examine your roof, mark damage with chalk, take photos and measurements, and inspect your attic and any interior damage. Let your contractor handle the technical discussion. Your job is to answer questions honestly, take notes, and make sure nothing gets overlooked.

Note: Never exaggerate damage: that’s fraud. But don’t let legitimate damage go undocumented either. Take your own photos during the inspection.

After the visit, the adjuster prepares an estimate outlining what they’ll cover. This usually arrives in one to two weeks and often comes in lower than your contractor’s estimate. That’s normal and expected.

Review And Supplement The Estimate

Here’s something most homeowners don’t know: insurance roof replacement estimates almost always leave things out. They might miss overhead and profit for your contractor, proper underlayment, code-required upgrades, permit fees, or disposal costs.

Sit down with your contractor and compare the insurance estimate to their estimate line by line. Look for missing items, undervalued materials, incorrect measurements, and omitted requirements.

In Southern California, pay special attention to cool roof requirements under California Title 24, wildfire-resistant materials if you’re in a high-risk zone, and proper tile roof specifications since tiles are common in our area.

You have the right to request a supplement, additional coverage beyond the initial estimate. This is your right as the policyholder, not something your contractor can do for you.

Create an itemized list of what’s missing, include your contractor’s justification for each item, attach supporting photos, and submit it in writing to your adjuster. The most commonly missed items are overhead and profit, code upgrades, proper underlayment, and complete flashing replacement.

Expect some back and forth. Your first supplement might get partially approved, requiring a second submission. Stay persistent but professional. This process can increase your payout by $3,000 to $8,000 or more.

Also, read:

- Moss And Algae Removal From Roofs

- Roof Maintenance: Essential Tasks For Longevity

- Complete Roof Inspection Guide For Homeowners

What To Expect From Your Insurance Payout

Understanding how your insurance pays out is key to avoiding surprises during your roof replacement. Whether you have an RCV or ACV policy, the number of payments, the timing, and even your mortgage lender’s involvement can all affect how quickly funds arrive. Here’s a clear breakdown of what to expect.

Replacement Cost Value (RCV) Policies

You’ll receive two payments under an RCV policy:

- Payment 1: Sent after claim approval. This check equals the replacement cost minus depreciation and your deductible, usually enough for your contractor’s deposit.

- Payment 2: Issued after the roof is fully replaced and verified. This covers any recoverable depreciation. Your contractor submits completion photos and a final invoice to trigger it.

If You Have a Mortgage

Insurance checks are made out to both you and your lender. Because lenders often hold funds in escrow and release them in stages, this can add 2–4 weeks to the timeline.

Actual Cash Value (ACV) Policies

ACV provides one payment: the depreciated value minus your deductible. It typically doesn’t cover full replacement costs, so homeowners pay the difference. We offer financing options with low monthly payments to help close that gap.

If Your Claim Is Denied

Denials happen even for legitimate damage. Common reasons include cosmetic damage, pre-existing issues, wear and tear, or roofs beyond the age limit.

If your claim is denied:

- Request the denial in writing.

- Ask for reconsideration with new evidence.

- Submit a formal appeal.

- Consult a public adjuster.

- File a complaint with the California Department of Insurance.

Sometimes denials are valid—especially for wear-and-tear damage. In those cases, financing options may be the best way out.

Getting insurance to pay for roof replacement takes effort, documentation, and persistence. But for most homeowners with legitimate storm damage and proper coverage, insurance will cover most or all of a quality roof replacement. The key is doing things in the right order:

Our 20 years of experience mean we know exactly what insurance companies look for and how to get insurance to pay for roof replacement when coverage is justified.

Schedule your free roof inspection today. We’ll assess your damage, review your policy with you, and help you understand whether filing a claim makes sense. If it doesn’t, we can help you repair your roof, and if you’re considering a more energy-efficient option, we also install cool roofs.

FAQs

Could filing a small repair claim lead to issues with a larger roof loss later?

Yes, if you file a roof insurance claim for minor damage without clear storm evidence, it can trigger elevated risk ratings or policy exclusions. That’s why learning how to get insurance to pay for roof starts with documenting damage properly and only filing when replacement looks justified.

How can I find out what kind of coverage my policy has without waiting for a claim?

Contact your insurer or agent and ask whether your policy answers “does homeowners insurance cover roof replacement or only pays out on a repair basis”. Knowing this ahead of time can save you from surprise costs or claim denial when you follow the process of how to get insurance to pay for roof replacement.

Are older roofs automatically excluded from coverage?

Not automatically, but age and maintenance history matter. Insurers may limit payments if your roof is old or poorly maintained. This means your insurance roof replacement payout could be for actual cash value rather than full replacement cost. Understanding this nuance is part of how to get insurance to pay for roof replacement.

Will insurance pay if the damage was there for months but only fixed now?

This is risky. If the insurer determines that gradual deterioration caused the issue rather than a specific event, they may deny the claim. So it’s essential to prove the damage was sudden and storm-related if you want to know “will insurance cover roof replacement under your policy”.

What does the question “Does homeowners’ insurance cover roof?” damage from trees mean?

If a tree falls and causes direct damage in a sudden event (like a storm), yes—your policy may pay for full replacement. But if the tree was leaning for years and finally fell due to decay or lack of maintenance, the insurer might classify it as excluded wear-and-tear. This difference plays a large role in how to get insurance to pay for roof replacement.

Related Posts

What Our Clients Say

Roof Replacement Inc. offers professional, high-quality work, guaranteed (call for details); ensuring all clients projects meet all code and design requirements. We are dedicated to exceptional customer service and will strive to ensure you with the highest quality roofing services. Roof Replacement Inc. offers lifetime warranty (call for details) on all of our workmanship to ensure the quality of our work. With over four decades of experience and success within the roofing and construction industry, Roof Replacement Inc. has grown and developed in all areas of roofing construction, including roof inspections. As a leading residential and commercial roofing company in LA, we have hundreds of references from previous clients, so rest assured, that your roofing job will be done right the first time. Replacing an old roof can help add curb appeal and will increase the perceived value of your home. First impressions are vital when selling your home, especially when your roof takes up more than half of the exterior of your residence or business. Not only is the return of investment on a new roof attractive for potential buyers, but can be as beneficial as remodeling the kitchen or bathrooms within your residence.